At the macro level, several trends either directly or indirectly impact downstream.

First is the evolving regulatory landscape, such as emissions trading schemes (ETS) and capping of greenhouse gases in a region. Or Carbon Pricing Mechanisms: adding a direct cost on carbon emissions, often through carbon taxes or carbon fees. And Fuel Economy Standards still play an active role.

Second is the energy transition and diversification into renewables like solar, wind, and biofuel. The Exxon Mobil 2023 acquisition of Denbury Resources in 2023 significantly enhanced their capabilities for transporting and storing captured CO2.

Third, geopolitical instability is causing a ripple effect through the industry by causing supply and price fluctuations. countries seek alternative oil suppliers, realigning global supply chains.

Heighten concerns about energy security, prompting countries to prioritize securing reliable sources of oil. And finally, BlackRock and Vanguard ( some of the largest investment firms with large stakes in oil and gas and chemicals) are adapting their ESG strategies in response to various market pressures and dynamics.

While they may not be moving as fast as some ESG advocates would like, they instead focus on Engagement engagement with companies in their portfolios. This entails pushing companies to improve their ESG practices through dialogue rather than immediate divestment.

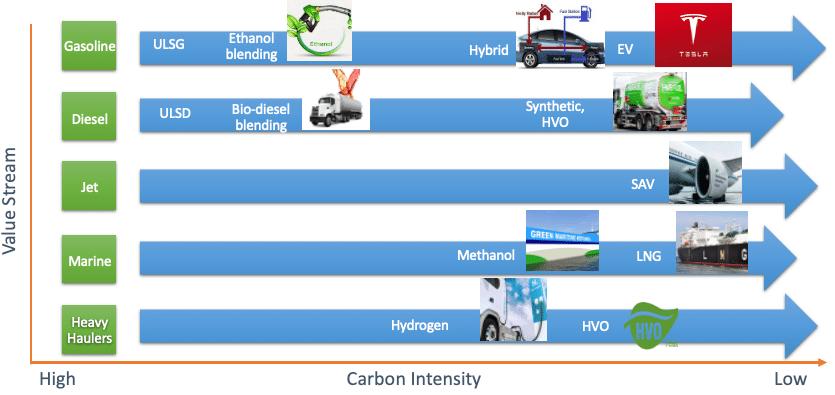

The future of transportation and decarbonization of the downstream is where things get interesting and are often debated. As a way of visualizing progress, many companies have abandoned the simplistic colours used to characterize, for example, green hydrogen and shifted to carbon intensity.

Carbon intensity refers to the amount of greenhouse gases (measured as carbon dioxide equivalent, or CO2e) emitted per unit of activity. It’s a metric to compare the environmental impact of different processes or products. If you consider each value stream, some have already progressed in lowering carbon intensity while others are just beginning, such as marine.

Ethanol and biodiesel have re-shaped refined products for decades, sustainable aviation fuel or Hydrotreated Vegetable Oil are promising, but scale availability of feedstocks and potential negative impact on plant ecosystems is yet to be determined. As for hydrogen home heat, the use of Hydrogen is likely a dead end. Applications are likely in heavy and marine goods transport via ammonia/ methanol and other proxies.

We know that, due to the second law of Thermodynamics, it is very difficult to make, store, and transport Hydrogen. This reality may NEVER be escaped. Hydrogen is also tricky due to safety and combustibility.

These factors make the Hydrogen future challenging to innovate and scale at best.

COP and CERAweek offered exciting perspectives. I won’t go in-depth into all of the differences in each event and what world leaders are saying at the most important events in our industry – I do want to highlight some important factors.

Overall, the COP seemed to focus on Fast-tracking the Energy Transition, fixing climate finance, accelerating investments in renewables, phasing out coal, developing clean energy technologies, and ensuring sufficient financial resources are available, particularly for developing countries. CERAWeek 2024 focused on the complexities of navigating a multidimensional energy transition.

Key themes that emerged were balancing urgency with reality and the growing recognition of concerns about ensuring energy security, affordability, and equitable access during the transition. It also highlighted The role of natural gas as a potential bridge fuel, and Developed new technologies like carbon capture and storage (CCUS).

Both events recognized Geopolitical considerations: Energy security concerns are back on the agenda, with the war in Ukraine highlighting the vulnerability of global energy supplies.